"Double Top" or Double Down?

"Double Top" or Double Down?

It's hard to see a looming recession, but it's harder to imagine setting new market records amid uncertainty around the pace of rate cuts and the election outcome

September brings the return school, a fresh flood of meetings and financial markets that keep everyone guessing. Earnings are healthy, policy looks set to ease and U.S. consumers are spending, but we've now had two sharp declines in two months for no obvious reason. Neither semiconductor weakness, nor South China Sea tensions, nor even slightly weaker data add up to a credible explanation this week.

So is this a hiccup or a dreaded “double top” that some chartists might signal as the beginning of the end? My answer is that it’s hard to envision a market meltdown from here, but setting lots of fresh record highs before year-end is even harder to see.

A few charts collected by our friends at The Daily Shot offer perspective:

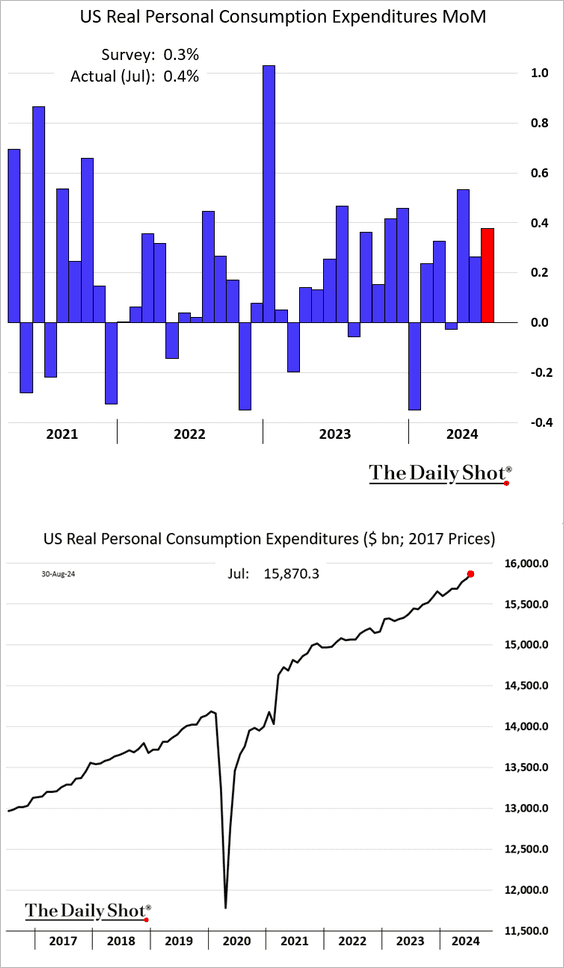

If you are looking for signs of the next downturn, you won’t find many in the behavior of America’s resolute shoppers. Yes, there is stress among lower-income households, but spending patterns look as strong as ever.

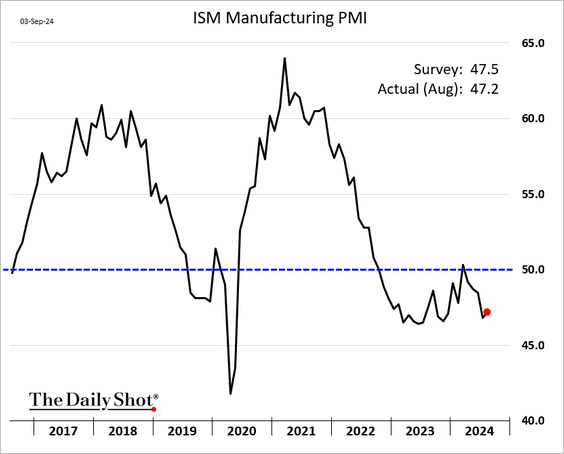

What seems to have spooked everyone this week are weaker manufacturing readings aggravated by mounting concerns about whether tech and semiconductor demand will be “super sky high” or merely “sky high.”

Recessions can come at you fast and the U.S. faces downdrafts from a softening construction sector and a string of regional banks overexposed to bad real estate loans. Still, there are few signs that the U.S. economy is unraveling, with the Atlanta Fed’s GDP Now Estimate still at a robust 2.0% for this quarter.

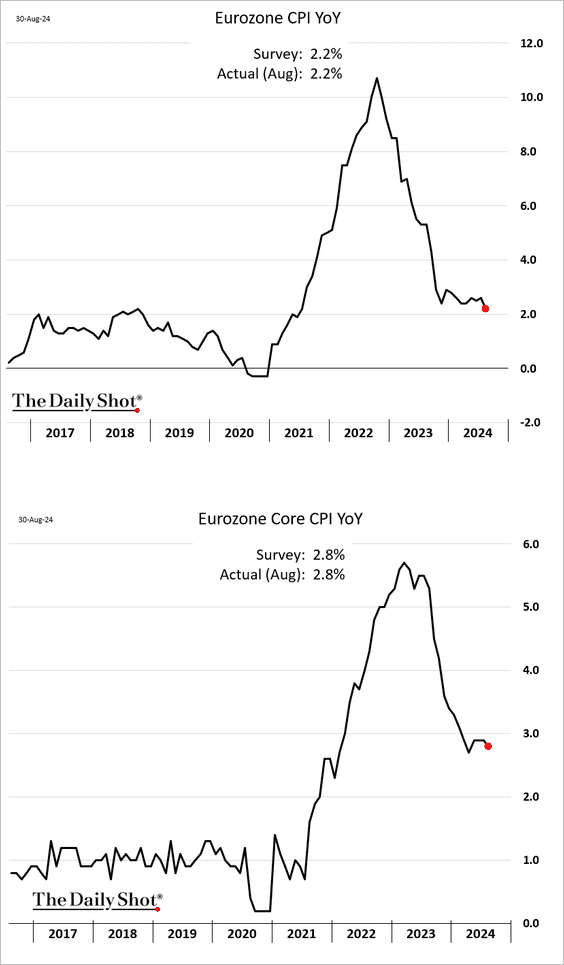

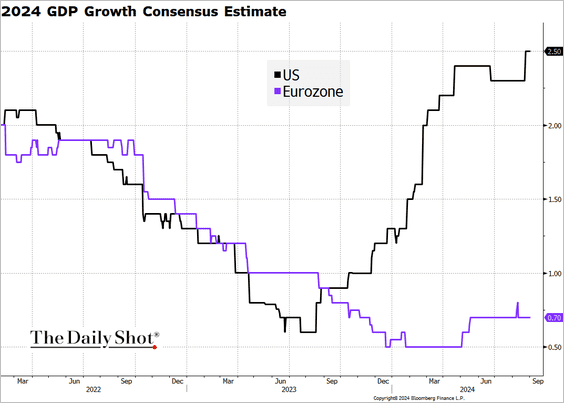

But not all is well beyond America’s shores. The European Central Bank has successfully brought inflation under control, but euro area growth remains deeply uninspiring.

Europe’s immediate challenges have to do with fiscal constraints in Germany and political chaos in France, but the region faces a long list of problems including weaker demand from China, high energy costs and deep-seated structural issues. It will be difficult for the European economy to surprise on the upside over the next year.

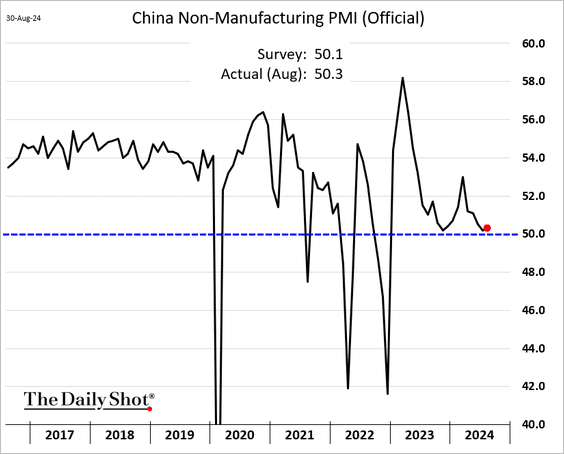

China might well surprise on the upside, but that’s only because expectations are still at rock bottom. Yes, Xi Jinping has promised to deliver growth of “about 5%,” which looks good by most standards, but there’s a dawning realization that Chinese growth will drop below 4% long before we see anything above 5% again soon.

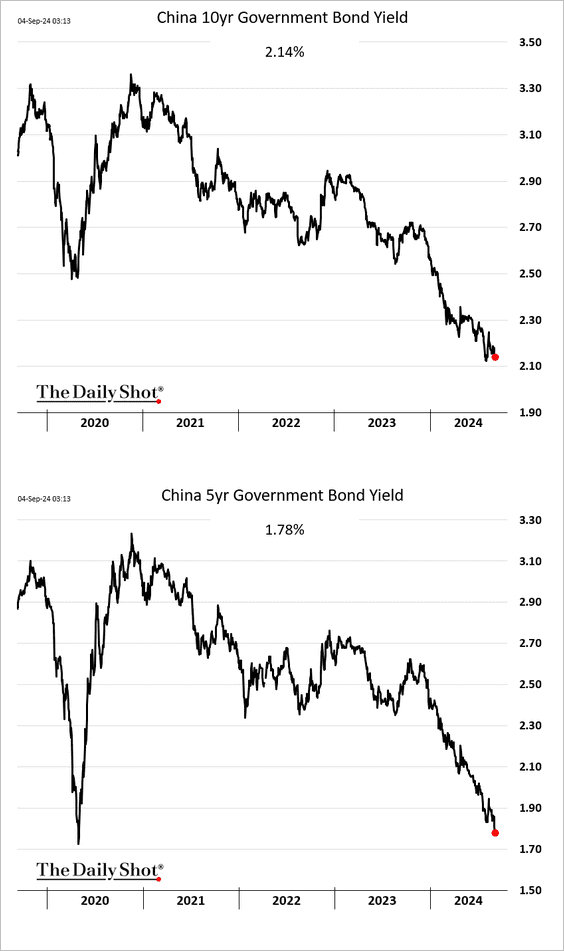

Falling bond yields are a sign that the hangover from China’s real estate bust continues to cast a cloud over consumer demand. So far, the government has offered little hope it will retool an economic model that favors industrial production (and exports) over consumption. At some point, Chinese financial markets could get a bounce simply because expectations are so low, but the overall trajectory is hardly promising.

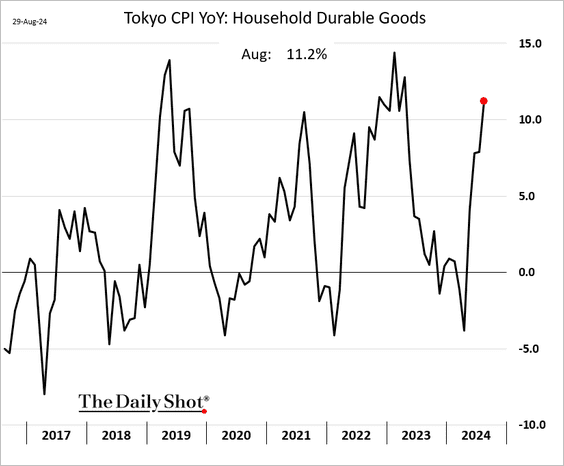

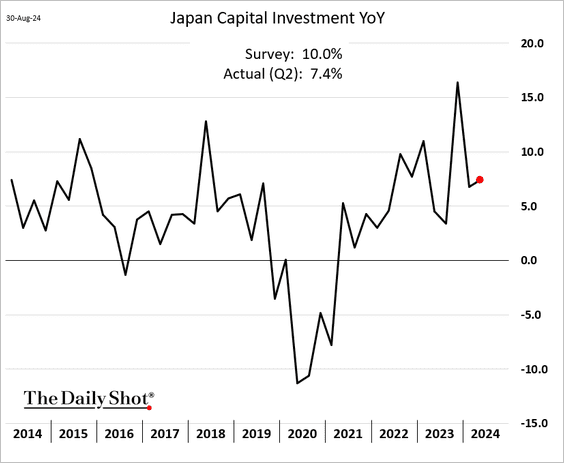

Investors rarely put “promising” and Japan in the same sentence, but recent inflation and growth data seem worth a closer look. Union negotiations should continue to drive wages higher, which will support more lasting services inflation. Expectations that Japanese deflation risks are past will also underpin healthier consumer demand. And with U.S. rate cuts ever closer, the yen should bounce back, too.

As always with Japan, however, the risk comes from policy. The country’s reflation story looks durable as long as the government debt worrywarts don’t rush to choke it off with higher taxes or interest rates.

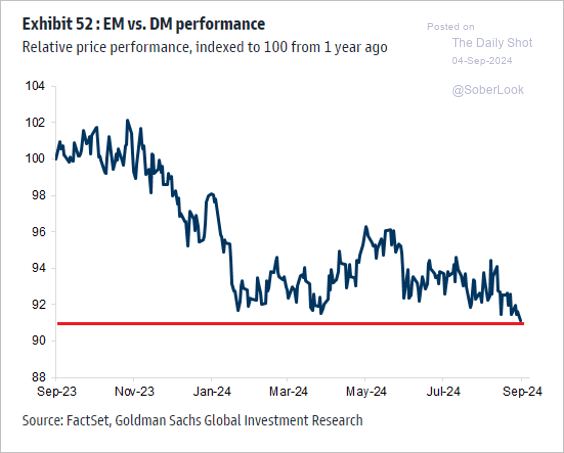

Further afield, many emerging markets look promising. India’s expansion continues at a healthy clip. Mexico offers considerable upside if the new government can take advantage of the mounting interest in “near-shoring” manufacturing destined for the United States. Even troubled South Africa may soon be worth a closer look as the new government explores market-friendly reforms.

But, of course, it’s hard for Emerging Markets to deliver much while the United States posts eye-watering returns at far lower risk, which leads us back to the initial question about this week’s air pocket. Is it an opportunity to buy on weakness or your chance to head for cash, gold and canned food.

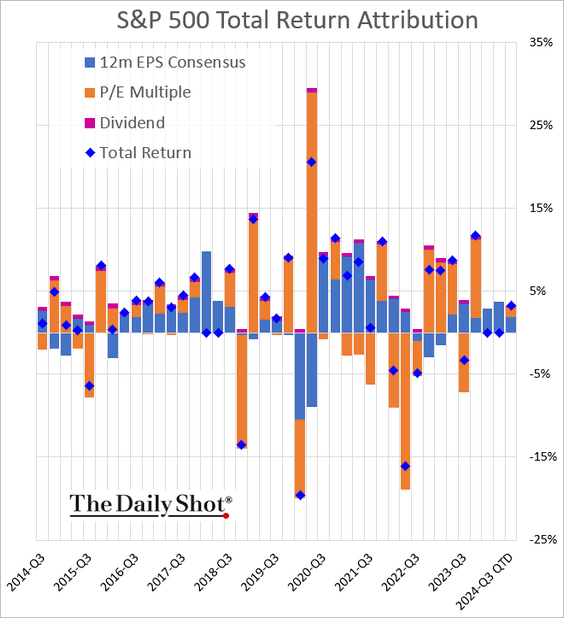

My answer is that the next U.S. recession is still hard to imagine over the next 12 months given what we know about household balance sheets, corporate earnings and the likelihood 150-200 bps in rate cuts by next summer. Recent stock returns have also been driven more by earnings growth than multiple expansion.

Still, if you look ahead to the fall, it seems too soon to double down on risk. There is still upside in value over growth and, maybe, cyclicals over technology stocks. But sentiment is clearly turning sour. Increasingly, investors raise more doubts about good data, fret about the neutral and dwell on the bad. Witness last week’s reaction to the only-slightly-less-than-stellar Nvidia results.

So brace for much confusion about the likely pace of Fed cuts and and buckle up for a tight U.S. election campaign that may shock the outlook from stiff new tariffs and immigration restrictions. Amid the market angst, this may just be one of those times when it makes sense to do nothing.