IMF to the Rescue!

IMF to the Rescue!

There was plenty of good advice for the world economy last week in Washington DC, but we may need help from the other team, too.

The mood in Washington, DC last week was decidedly bullish on the outlook for the U.S. economy and bearish on just about everything else, including rising debt levels, falling growth rates and the fate of the world. Investors who joined the assembled officials at the International Monetary Fund and World Bank Spring Meetings were too nervous to be shorting the market even as it sold off, but more than a few were looking for exits if the ride gets much bumpier.

And with conversations more focused on Ukrainian ammunition supplies, Iranian drone attacks and South China Sea collisions, it would be reassuring to know we could expect help from the Impossible Mission Force in addition to the folks who wrote the latest World Economic Outlook which argued this last year hasn’t been as bad as it feels.

It’s worth quoting at length from a document that so normally reads like it’s co-authored by Eeyore and Chicken Little.

“The global economy remains remarkably resilient, with growth holding steady as inflation returns to target. The journey has been eventful, starting with supply-chain disruptions in the aftermath of the pandemic, a Russian-initiated war on Ukraine that triggered a global energy and food crisis, and a considerable surge in inflation, followed by a globally synchronized monetary policy tightening.

“Yet, despite many gloomy predictions, the world avoided a recession, the banking system proved largely resilient, and major emerging market economies did not suffer sudden stops. Moreover, the inflation surge—despite its severity and the associated cost-of living crisis—did not trigger uncontrolled wage-price spirals. Instead, almost as quickly as global inflation went up, it has been coming down. … Most indicators point to a soft landing.”

If there was broad agreement that the IMF’s economic remedies are on target, there was also consensus that the odds of implementation are low.

But what’s done is done and the assembled economists and investors understood all too well that markets price in very mixed expectations of the future.

Topping economic concerns is the ocean of government debt that looks likely to grow significantly over the next decade to pay for climate transition, military modernization and the health care of aging populations. This spending will come on top of debt levels that are already too high and will be difficult for even the most committed deficit hawks to hold back.

All eyes are focused on the United States next year when tax cuts enacted under President Donald Trump in 2017 are set to expire. Should he be back in office by then, observers are scratching their heads at the potential impact of his promises to further reduce taxes, raise tariffs and restrict immigration. All of these seem broadly inflationary and likely to keep the long end of the curve higher even if the Fed manages to start cutting rates over the summer as most still expect.

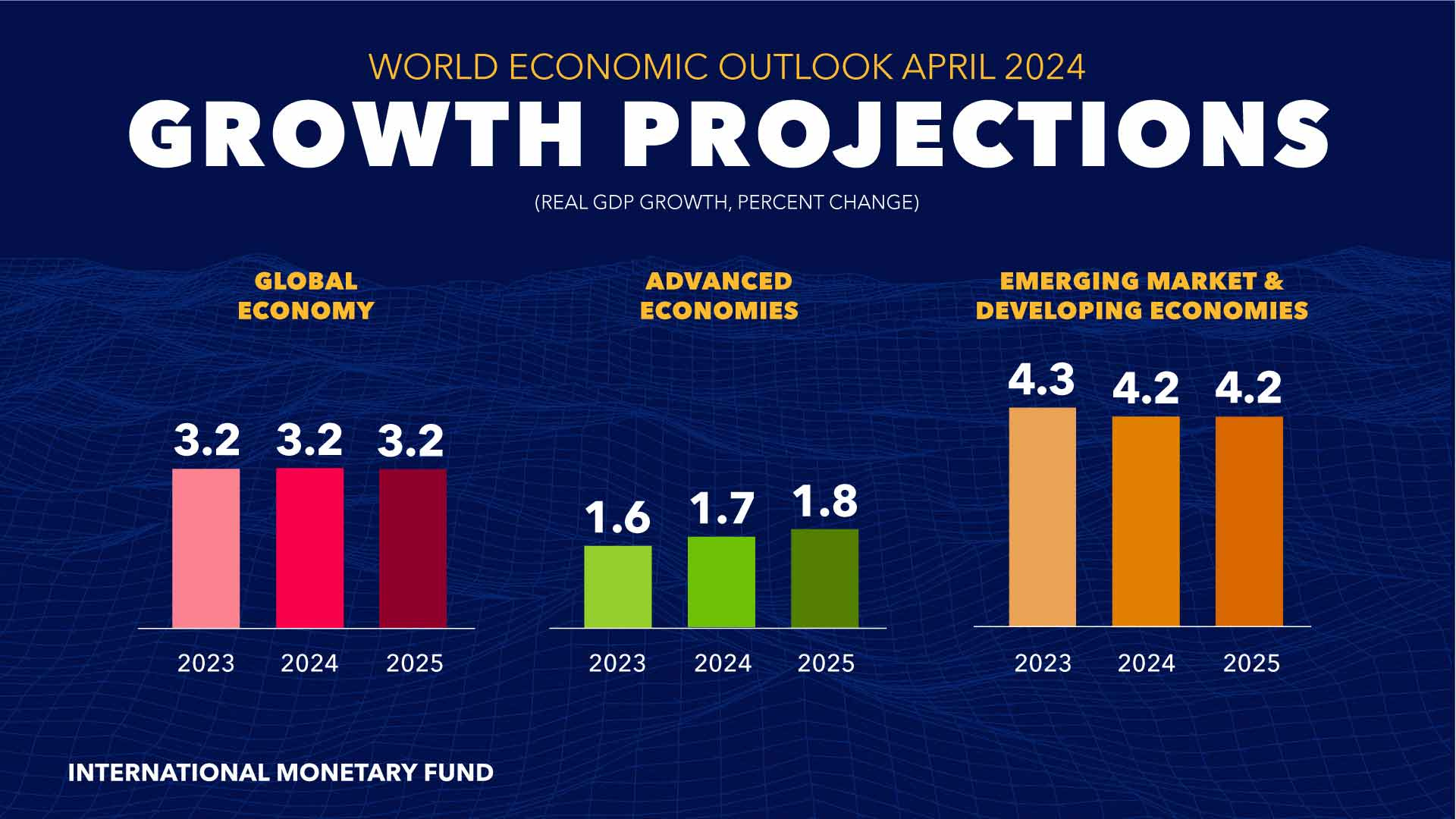

If government debts are rising, growth is falling. The IMF projects the global economy will expand this year by 3.2%, which reflects better prospects for the U.S. and a mostly worse outlook everywhere else. Indeed, 3.2% is last year’s actual number and next year’s forecast. The projection for growth in five years is 3.1%, the lowest such forecast in decades, which prompted the IMF to reiterate its plea for policies to address declining productivity, misallocated capital and fragmenting supply chains.

Also worrying is the widening gap between rich and poor, as low-income countries seem to have been left with deeper pandemic scars. Here the IMF urges governments to accelerate structural reforms that will attract more investment and do much more to provide training to the rapidly expanding cohorts of younger workers.

Drowning out most discussions of debt and growth last week, however, were dire concerns about geopolitical risk. There was plenty of talk about the open warfare between Iran and Israel that gave oil markets a jolt even if all the main players want to protect energy markets. Ukraine’s perilous position had many Europeans wondering aloud if U.S. security guarantees mean anything anymore.

Surprisingly, U.S.-China tensions were lower on the list as the rhetoric between Washington and Beijing has calmed. But there was lots of talk about the costs of building resilient supply chains and the future of free trade as voters choose to press concerns for national security and protection at the expense of economic efficiency and growth. These are choices that mostly flout anything the IMF has ever recommended and create risks that are fiendishly difficult for market to price in.

For investors, the consensus last week was that the robust U.S. economy means higher rates for longer, a stronger dollar for longer and emerging market risks that remain too high even if stock valuations and bond spreads seem tempting.

If there was broad agreement that the IMF’s economic remedies are on target, there was also consensus that the odds of implementation are low. Meanwhile, the world remains a treacherous place, unless Tom Cruise and team can ease the geopolitical risks with an impossible mission or two.

Unfortunately, even the US got its share of finger pointing. Fiscal profligacy-financed private demand growth now creates a public debt management challenge to the point of triggering frequent headlines like "2-year (US Treasuries) auction better than feared". Wouldn't it be ironic that a US downgrade, no matter its fairness, added to the world's miseries? As for finding the right fiscal framework, plus ça change...