More Than Just the Yips

As market doubts about the dollar’s status rise, investors should start contemplating a confusing world of competing safe havens.

If ever there were a country that needed to borrow at preferential interest rates, it’s the United States with its mounting debts, aging demographics and evaporating fiscal discipline. If ever there were a country deliberately undermining the reserve currency status that keeps its borrowing costs low, it’s the United States with its selfish trade agenda, overreaching sanctions and poisonous politics.

With China unwilling to take the steps required for the yuan to replace the dollar and Europe unable to do what needs to be done on behalf of the euro, the global financial system looks headed to a long and slow unravelling. This will take a long time, but the current trajectory looks headed to a multi-currency world without a global lender of last resort and few certain places to hide in a crisis.

For all the debate on the dollar’s decline, of course, it still accounts for 57% of the global reserves, 54% of export invoicing and 88% of foreign exchange transactions. As long as commodity derivatives are mainly priced in dollars and Hollywood crooks still measure their loot in America’s currency, there’s a long way to go before the dollar’s dominance fades. But investors should start to imagine a world in which dollar, yuan and euro coexist with more equal reach.

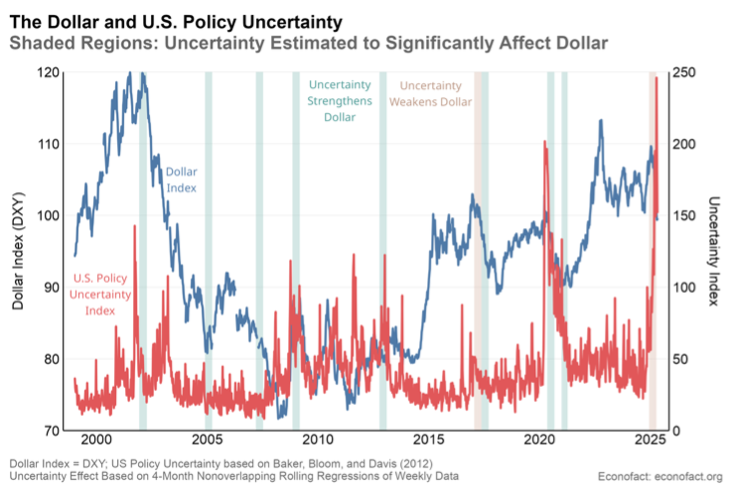

I have made my own contributions to a vast literature of angst and woe around America’s self-destructive behavior and the risks ahead, including here, here and here. But a shrewd analysis by my former Treasury colleagues Charles Collyns and Michael Klein confirms the angst in numbers. In a fresh addition to the must-read analytical blog Econofact, they examine 10 events since the late 1990s when a spike in policy uncertainty led to a flight to safety that strengthened the dollar against other currencies. They find, however, that in two recent such moments, both coinciding with the start of Donald Trump’s two terms, the opposite is true.

You may scoff that’s only two data points, but it's enough to wonder if that blood-curdling selloff in stocks, bonds and the dollar that followed “Liberation Day” was an aberration. Trump wrote it off as market “yips.” Collyns and Klein suggest that the “dollar smile,” a market phenomenon in which the dollar strengthens in both good times and bad, may be turning into a frown. Stay tuned.

Meanwhile, consider two other currencies that have actual plans in place to extend their reach for both economic and geopolitical purposes.

China has been deliberately boosting the internationalization of its currency. The Belt and Road Initiative builds infrastructure with loans denominated in yuan, while a network of currency swap lines helps prime the pump for Chinese currency flows globally. The digital yuan is at the forefront of modernizing payment systems that will surely fuel adoption overseas.

But even as the largest trading partner for 120 countries, China can’t expect broad use of its currency as long as it’s not freely convertible. And even if Xi Jinping or his successors take this bold step someday, the absence of independent regulators in a single-party system means that anyone holding a yuan will wonder when the rules might change again.

If China may be unwilling to take the required steps to make its currency convertible, Europe looks unable. Last month, European Central Bank President Christine Lagarde outlined the concrete steps ahead for the euro to become a more reliable global currency that would reduce Europe’s borrowing rates, insulate European businesses from exchange rate volatility and reduce the continent’s geopolitical dependence on an increasingly unpredictable America.

You may scoff that’s only two data points, but it's enough to wonder if that blood-curdling selloff in stocks, bonds and the dollar that followed “Liberation Day” was an aberration. Trump wrote it off as market “yips.”

The problem is that many of her steps depend on some magical thinking about domestic politics in places like France, Germany and Italy. “A steadfast commitment to open trade” and “deeper and more liquid capital markets” look well within reach. But “underpinning [trade] with security capabilities” and “uniting politically so that we can resist external pressures” sound far-fetched at best.

All this means we may be headed for a much more confusing monetary world. Hélène Rey of the London Business School makes her own case for the euro, but also reminds us of the theory of hegemonic stability advanced in Charles P. Kindelberger’s study of the Great Depression. An open and stable international system, in this view, depends on a single great power.

Imagine a crisis in which no single central bank can restore liquidity and confidence to markets. Worse, imagine if two or three central banks try to secure leverage by making their liquidity conditional. Or perhaps they just miscalculate and miscommunicate, leaving investors scurrying for hiding places in cryptocurrency and precious metals.

We may still be a long way from such a world, but the closer we approach, the rougher the ride will be.

Could not agree more. If the USD does lose its primacy (and we're doing our best to see if that can be achieved), we will not find ourselves in today's world with the euro or renminbi having replaced the dollar -- we will find ourselves in a very different world, with a choice of different unsafe havens.