This Week's Chart, Next Week's Markets

Past vs. Future, European inflation, Chinese growth, Japanese recovery, U.S. jobs

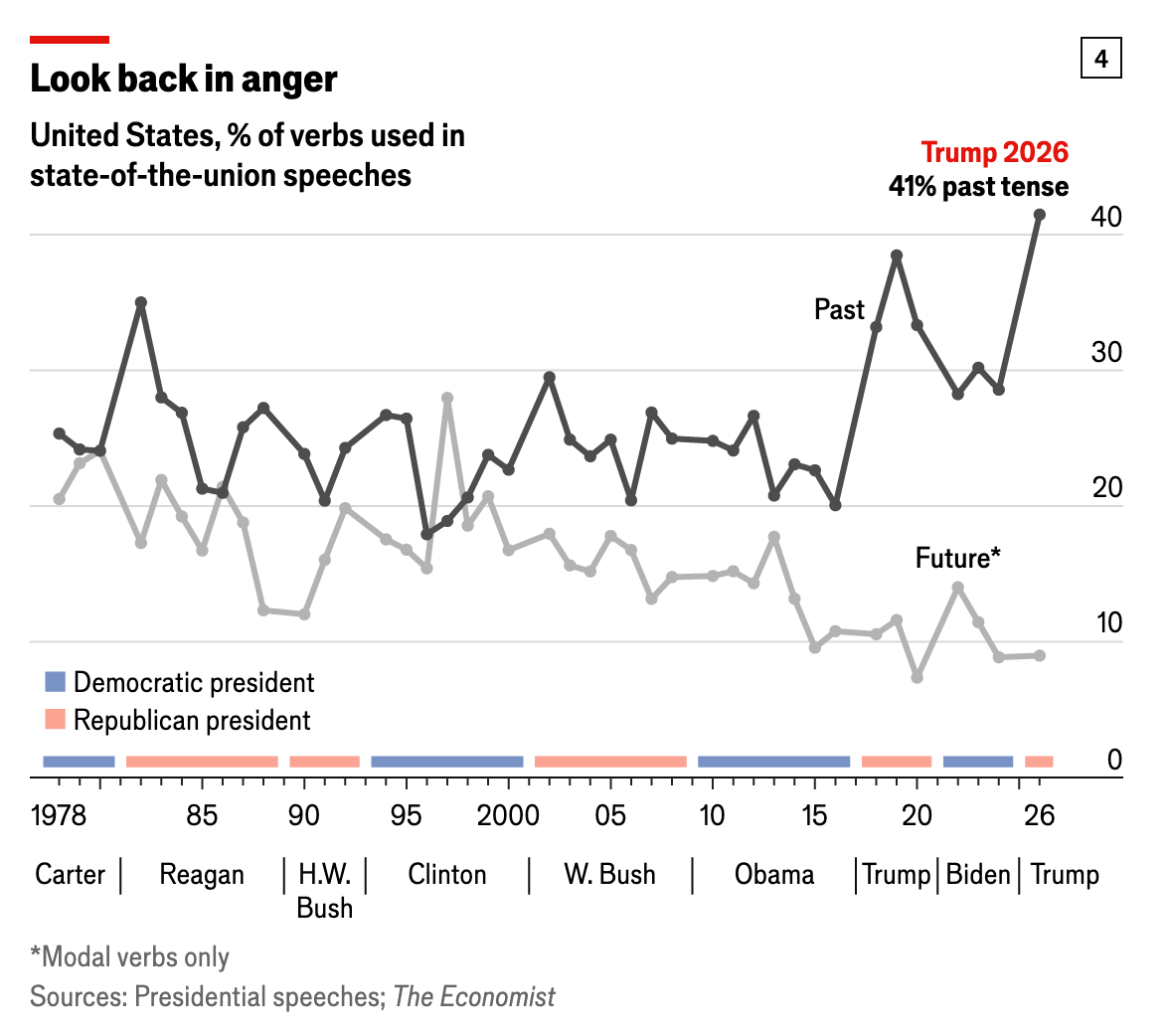

We have all noticed that President Trump speaks more of America’s past greatness than its prospects for a better future. But The Economist suggests that State of the Union addresses have focused less and less on the path ahead for at least five decades. Was Ronald Reagan more stuck in the past than Jimmy Carter? Was Bill Clinton so much more forward-thinking than George W. Bush? Plenty of material for political scholars to dissect, but investors might also ask why they should risk money in a country that spends so much time talking about the old days.

Meanwhile, take a quick peek ahead at what may move next week’s markets.

Tuesday: The euro area flash estimate for Consumer Price Inflation should come in close to 1.8%, raising the odds of a mid-year rate cut by the European Central Bank.

Wednesday: Japan’s Leading Economic Index could show even further strength, raising the odds of a stronger yen and earlier rate hikes.

Wednesday: China opens a series of key meetings that will adopt the 15th Five-Year Plan and approve a growth target for this year. Anything less that 5% would suggest the leaders are focused more on structural reforms than short-term stimulus.

Friday: U.S. Non-Farm Payrolls for February will need to come in lower than the last reading of 130,000 jobs, or markets will start pushing out the next rate cuts to the fall, with or without Kevin Warsh.